I don’t yet have actual words committed to text editor for this year’s little A-to-Z yet. Soon, though. Rather than leave things completely silent around here, I’d like to re-share an old sequence about something which delighted me. A lon while ago I read Edmund Callis Berkeley’s Giant Brains: Or Machines That Think. It’s a book from 1949 about numerical computing. And it explained just how to really calculate logarithms.

Anyone who knows calculus knows, in principle, how to calculate a logarithm. I mean as in how to get a numerical approximation to whatever the log of 25 is. If you didn’t have a calculator that did logarithms, but you could reliably multiply and add numbers? There’s a polynomial, one of a class known as Taylor Series, that — if you add together infinitely many terms — gives the exact value of a logarithm. If you only add a finite number of terms together, you get an approximation.

That suffices, in principle. In practice, you might have to calculate so many terms and add so many things together you forget why you cared what the log of 25 was. What you want is how to calculate them swiftly. Ideally, with as few calculations as possible. So here’s a set of articles I wrote, based on Berkeley’s book, about how to do that.

Machines That Give You Logarithms explains how to use those tools. And lays out how to get the base-ten logarithm for most numbers that you would like with a tiny bit of computing work. I showed off an example of getting the logarithm of 47.2286 using only three divisions, four additions, and a little bit of looking up stuff.

Without Machines That Think About Logarithms closes it out. One catch with the algorithm described is that you need to work out some logarithms ahead of time and have them on hand, ready to look up. They’re not ones that you care about particularly for any problem, but they make it easier to find the logarithm you do want. This essay talks about which logarithms to calculate, in order to get the most accurate results for the logarithm you want, using the least custom work possible.

And that’s the series! With that, in principle, you have a good foundation in case you need to reinvent numerical computing.

GoldenOj suggested the exponential as a topic. It seemed like a good important topic, but one that was already well-explored by other people. Then I realized I could spend time thinking about something which had bothered me.

In here I write about “the” exponential, which is a bit like writing about “the” multiplication. We can talk about and and many other such exponential functions. One secret of algebra, not appreciated until calculus (or later), is that all these different functions are a single family. Understanding one exponential function lets you understand them all. Mathematicians pick one, the exponential with base e, because we find that convenient. e itself isn’t a convenient number — it’s a bit over 2.718 — but it has some wonderful properties. When I write “the exponential” here, I am looking at this function where we look at .

This piece will have a bit more mathematics, as in equations, than usual. If you like me writing about mathematics more than reading equations, you’re hardly alone. I recommend letting your eyes drop to the next sentence, or at least the next sentence that makes sense. You should be fine.

My professor for real analysis, in grad school, gave us one of those brilliant projects. Starting from the definition of the logarithm, as an integral, prove at least thirty things. They could be as trivial as “the log of 1 is 0”. They could be as subtle as how to calculate the log of one number in a different base. It was a great project for testing what we knew about why calculus works.

And it gives me the structure to write about the exponential function. Anyone reading a pop-mathematics blog about exponentials knows them. They’re these functions that, as the independent variable grows, grow ever-faster. Or that decay asymptotically to zero. Some readers know that, if the independent variable is an imaginary number, the exponential is a complex number too. As the independent variable grows, becoming a bigger imaginary number, the exponential doesn’t grow. It oscillates, a sine wave.

That’s weird. I’d like to see why that makes sense.

To say “why” this makes sense is doomed. It’s like explaining “why” 36 is divisible by three and six and nine but not eight. It follows from what the words we have mean. The “why” I’ll offer is reasons why this strange behavior is plausible. It’ll be a mix of deductive reasoning and heuristics. This is a common blend when trying to understand why a result happens, or why we should accept it.

I’ll start with the definition of the logarithm, as used in real analysis. The natural logarithm, if you’re curious. It has a lot of nice properties. You can use this to prove over thirty things. Here it is:

The “s” is a dummy variable. You’ll never see it in actual use.

So now let me summon into existence a new function. I want to call it g. This is because I’ve worked this out before and I want to label something else as f. There is something coming ahead that’s a bit of a syntactic mess. This is the best way around it that I can find.

Here, ‘c’ is a constant. It might be real. It might be imaginary. It might be complex. I’m using ‘c’ rather than ‘a’ or ‘b’ so that I can later on play with possibilities.

So the alert reader noticed that g(x) here means “take the logarithm of x, and divide it by a constant”. So it does. I’ll need two things built off of g(x), though. The first is its derivative. That’s taken with respect to x, the only variable. Finding the derivative of an integral sounds intimidating but, happy to say, we have a theorem to make this easy. It’s the Fundamental Theorem of Calculus, and it tells us:

We can use the ‘ to denote “first derivative” if a function has only one variable. Saves time to write and is easier to type.

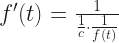

The other thing that I need, and the thing I really want, is the inverse of g. I’m going to call this function f(t). A more common notation would be to write but we already have in the works here. There is a limit to how many little one-stroke superscripts we need above g. This is the tradeoff to using ‘ for first derivatives. But here’s the important thing:

Here, we have some extratextual information. We know the inverse of a logarithm is an exponential. We even have a standard notation for that. We’d write

in any context besides this essay as I’ve set it up.

What I would like to know next is: what is the derivative of f(t)? This sounds impossible to know, if we’re thinking of “the inverse of this integration”. It’s not. We have the Inverse Function Theorem to come to our aid. We encounter the Inverse Function Theorem briefly, in freshman calculus. There we use it to do as many as two problems and then hide away forever from the Inverse Function Theorem. (This is why it’s not mentioned in my quick little guide to how to take derivatives.) It reappears in real analysis for this sort of contingency. The inverse function theorem tells us, if f the inverse of g, that:

That g'(f(t)) means, use the rule for g'(x), with f(t) substituted in place of ‘x’. And now we see something magic:

And that is the wonderful thing about the exponential. Its derivative is a constant times its original value. That alone would make the exponential one of mathematics’ favorite functions. It allows us, for example, to transform differential equations into polynomials. (If you want everlasting fame, albeit among mathematicians, invent a new way to turn differential equations into polynomials.) Because we could turn, say,

into

and then

by supposing that f(t) has to be for the correct value of c. Then all you need do is find a value of ‘c’ that makes that last equation true.

Supposing that the answer has this convenient form may remind you of searching for the lost keys over here where the light is better. But we find so many keys in this good light. If you carry on in mathematics you will never stop seeing this trick, although it may be disguised.

In part because it’s so easy to work with. In part because exponentials like this cover so much of what we might like to do. Let’s go back to looking at the derivative of the exponential function.

There are many ways to understand what a derivative is. One compelling way is to think of it as the rate of change. If you make a tiny change in t, how big is the change in f(t)? So what is the rate of change here?

We can pose this as a pretend-physics problem. This lets us use our physical intuition to understand things. This also is the transition between careful reasoning and ad-hoc arguments. Imagine a particle that, at time ‘t’, is at the position . What is its velocity? That’s the first derivative of its position, so, .

If we are using our physics intuition to understand this it helps to go all the way. Where is the particle? Can we plot that? … Sure. We’re used to matching real numbers with points on a number line. Go ahead and do that. Not to give away spoilers, but we will want to think about complex numbers too. Mathematicians are used to matching complex numbers with points on the Cartesian plane, though. The real part of the complex number matches the horizontal coordinate. The imaginary part matches the vertical coordinate.

So how is this particle moving?

To say for sure we need some value of t. All right. Pick your favorite number. That’s our t. f(t) follows from whatever your t was. What’s interesting is that the change also depends on c. There’s a couple possibilities. Let me go through them.

First, what if c is zero? Well, then the definition of g(t) was gibberish and we can’t have that. All right.

What if c is a positive real number? Well, then, f'(t) is some positive multiple of whatever f(t) was. The change is “away from zero”. The particle will push away from the origin. As t increases, f(t) increases, so it pushes away faster and faster. This is exponential growth.

What if c is a negative real number? Well, then, f'(t) is some negative multiple of whatever f(t) was. The change is “towards zero”. The particle pulls toward the origin. But the closer it gets the more slowly it approaches. If t is large enough, f(t) will be so tiny that is too small to notice. The motion declines into imperceptibility.

What if c is an imaginary number, though?

So let’s suppose that c is equal to some real number b times , where .

I need some way to describe what value f(t) has, for whatever your pick of t was. Let me say it’s equal to , where and are some real numbers whose value I don’t care about. What’s important here is that .

And, then, what’s the first derivative? The magnitude and direction of motion? That’s easy to calculate; it’ll be . This is an interesting complex number. Do you see what’s interesting about it? I’ll get there next paragraph.

So f(t) matches some point on the Cartesian plane. But f'(t), the direction our particle moves with a small change in t, is another poiat whatever complex number f'(t) is as another point on the plane. The line segment connecting the origin to f(t) is perpendicular to the one connecting the origin to f'(t). The ‘motion’ of this particle is perpendicular to its position. And it always is. There’s several ways to show this. An easy one is to just pick some values for and and b and try it out. This proof is not rigorous, but it is quick and convincing.

If your direction of motion is always perpendicular to your position, then what you’re doing is moving in a circle around the origin. This we pick up in physics, but it applies to the pretend-particle moving here. The exponentials of and and will all be points on a locus that’s a circle centered on the origin. The values will look like the cosine of an angle plus times the sine of an angle.

And there, I think, we finally get some justification for the exponential of an imaginary number being a complex number. And for why exponentials might have anything to do with cosines and sines.

You might ask what if c is a complex number, if it’s equal to for some real numbers a and b. In this case, you get spirals as t changes. If a is positive, you get points spiralling outward as t increases. If a is negative, you get points spiralling inward toward zero as t increases. If b is positive the spirals go counterclockwise. If b is negative the spirals go clockwise. is the same as .

This does depend on knowing the exponential of a sum of terms, such as of , is equal to the product of the exponential of those terms. This is a good thing to have in your portfolio. If I remember right, it comes in around the 25th thing. It’s an easy result to have if you already showed something about the logarithms of products.

I got to remembering an old sequence of mine, and wanted to share it for my current audience. A couple years ago I read a 1949-published book about numerical computing. And it addressed a problem I knew existed but hadn’t put much thought into. That is, how to calculate the logarithm of a number? Logarithms … well, we maybe don’t need them so much now. But they were indispensable for computing for a very long time. They turn the difficult work of multiplication and division into the easier work of addition and subtraction. They turn the really hard work of exponentiation into the easier work of multiplication. So they’re great to have. But how to get them? And, particularly, how to get them if you have a computing device that’s able to do work, but not very much work?

Machines That Think About Logarithms sets out the question, including mentioning Edmund Callis Berkeley’s book that got me started on this. And some talk about the kinds of logarithms and why we use each of them.

Machines That Do Something About Logarithms sets out some principles. These are all things that are generically true about logarithms, including about calculating logarithms. They’re just the principles that were put into clever play by Harvard’s IBM Automatic Sequence-Controlled Calculator in the 1940s.

Machines That Give You Logarithms explains how to use those tools. And lays out how to get the base-ten logarithm for most numbers that you would like with a tiny bit of computing work. I showed off an example of getting the logarithm of 47.2286 using only three divisions, four additions, and a little bit of looking up stuff.

Without Machines That Think About Logarithms closes out the cycle. One catch with the algorithm described is that you need to work out some logarithms ahead of time and have them on hand, ready to look up. They’re not ones that you care about particularly for any problem, but they make it easier to find the logarithm you do want. This essay talks about which logarithms to calculate, in order to get the most accurate results for the logarithm you want, using the least custom work possible.

And there we go. Logarithms are still indispensable for mathematical work, although I realize not so much because we ever care what the logarithm of 47.2286 or any other arbitrary number is. Logarithms have some nice analytic properties, though, and they make other work easier to do. So they’re still in use, but for different problems.

Comic Strip Master Command decreed that this should be a slow week. The greatest bit of mathematical meat came at the start, with a Garfield that included a throwaway mathematical puzzle. It didn’t turn out the way I figured when I read the strip but didn’t actually try the puzzle.

Jim Davis’s Garfield for the 3rd is a mathematics cameo. Working out a problem is one more petty obstacle in Jon’s day. Working out a square root by hand is a pretty good tedious little problem to do. You can make an estimate of this that would be not too bad. 324 is between 100 and 400. This is worth observing because the square root of 100 is 10, and the square root of 400 is 20. The square of 16 is 256, which is easy for me to remember because this turns up in computer stuff a lot. But anyway, numbers from 300 to 400 have square roots that are pretty close to but a little less than 20. So expect a number between 17 and 20.

But after that? … Well, it depends whether 324 is a perfect square. If it is a perfect square, then it has to be the square of a two-digit number. The first digit has to be 1. And the last digit has to be an 8, because the square of the last digit is 4. But that’s if 324 is a perfect square, which it almost certainly is … wait, what? … Uh .. huh. Well, that foils where I was going with this, which was to look at a couple ways to do square roots.

One is to start looking at factors. If a number is equal to the product of two numbers, then its square root is the product of the square roots of those numbers. So dividing your suspect number 324 by, say, 4 is a great idea. The square root of 324 would be 2 times the square root of whatever 324 ÷ 4 is. Turns out that’s 81, and the square root of 81 is 9 and there we go, 18 by a completely different route.

So that works well too. If it had turned out the square root was something like then we get into tricky stuff. One response is to leave the answer like that: is exactly the square root of 328. But I can understand someone who feels like they could use a numerical approximation, so that they know whether this is bigger than 19 or not. There are a bunch of ways to numerically approximate square roots. Last year I worked out a way myself, one that needs only a table of trigonometric functions to work out. Tables of logarithms are also usable. And there are many methods, often using iterative techniques, in which you make ever-better approximations until you have one as good as your situation demands.

Anyway, I’m startled that the cheese doodles price turned out to be a perfect square (in cents). Of course, the comic strip can be written to have any price filled in there. The joke doesn’t depend on whether it’s easy or hard to take the square root of 324. But that does mean it was written so that the problem was surprisingly doable and I’m amused by that.

Ryan North’s Dinosaur Comics for the 4th goes in some odd directions. But it’s built on the wonder of big numbers. We don’t have much of a sense for how big truly large numbers. We can approach pieces of that, such as by noticing that a billion seconds is a bit more than thirty years. But there are a lot of truly staggeringly large numbers out there. Our basic units for things like distance and mass and quantity are designed for everyday, tabletop measurements. The numbers don’t get outrageously large. Had they threatened to, we’d have set the length of a meter to be something different. We need to look at the cosmos or at the quantum to see things that need numbers like a sextillion. Or we need to look at combinations and permutations of things, but that’s extremely hard to do.

Tom Horacek’s Foolish Mortals for the 4th is a marginal inclusion for this week’s strips, but it’s a low-volume week. The intended joke is just showing off a “tube sock” and an “inner tube sock”. But it happens to depict these as a cylinder and a torus and those are some fun shapes to play with. Particularly, consider this: it’s easy to go from a flat surface to a cylinder. You know this because you can roll a piece of paper up and get a good tube. And it’s not hard to imagine going from a cylinder to a torus. You need the cylinder to have a good bit of give, but it’s easy to imagine stretching it around and taping one end to the other. But now you’ve got a shape that is very different from a sheet of paper. The four-color map theorem, for example, no longer holds. You can divide the surface of the torus so it needs at least seven colors.

Mastroianni and Hart’s B.C. for the 5th is a bit of wordplay. As I said, this was a low-volume week around here. The word “logarithm” derives, I’m told, from the modern-Latin ‘logarithmus’. John Napier, who advanced most of the idea of logarithms, coined the term. It derives from ‘logos’, here meaning ‘ratio’, and ‘re-arithmos’, meaning ‘counting number’. The connection between ratios and logarithms might not seem obvious. But suppose you have a couple of numbers, and we’ll reach deep into the set of possible names and call them a, b, and c. Suppose a ÷ b equals b ÷ c. Then the difference between the logarithm of a and the logarithm of b is the same as the difference between the logarithm of b and the logarithm of c. This lets us change calculations on numbers to calculations on the ratios between numbers and this turns out to often be easier work. Once you’ve found the logarithms. That can be tricky, but there are always ways to do it.

Bill Rechin’s Crock for the 8th is not quite a bit of wordplay. But it mentions fractions, which seem to reliably confuse people. Otis’s father is helpless to present a concrete, specific example of what fractions mean. I’d probably go with change, or with slices of pizza or cake. Something common enough in a child’s life.

These are all the mathematically-themed comic strips for the past week. Next Sunday, I hope, I’ll have more. Meanwhile please come around here this week to see what, if anything, I think to write about.

I’m back to requests! Today’s comes from commenter Dina Yagodich. I don’t know whether Yagodich has a web site, YouTube channel, or other mathematics-discussion site, but am happy to pass along word if I hear of one.

Let me start by explaining integral calculus in two paragraphs. One of the things done in it is finding a `definite integral’. This is itself a function. The definite integral has as its domain the combination of a function, plus some boundaries, and its range is numbers. Real numbers, if nobody tells you otherwise. Complex-valued numbers, if someone says it’s complex-valued numbers. Yes, it could have some other range. But if someone wants you to do that they’re obliged to set warning flares around the problem and precede and follow it with flag-bearers. And you get at least double pay for the hazardous work. The function that gets definite-integrated has its own domain and range. The boundaries of the definite integral have to be within the domain of the integrated function.

For real-valued functions this definite integral has a great physical interpretation. A real-valued function means the domain and range are both real numbers. You see a lot of these. Call the function ‘f’, please. Call its independent variable ‘x’ and its dependent variable ‘y’. Using Euclidean coordinates, or as normal people call it “graph paper”, draw the points that make true the equation “y = f(x)”. Then draw in the x-axis, that is, the points where “y = 0”. The boundaries of the definite integral are going to be two values of ‘x’, a lower and an upper bound. Call that lower bound ‘a’ and the upper bound ‘b’. And heck, call that a “left boundary” and a “right boundary”, because … I mean, look at them. Draw the vertical line at “x = a” and the vertical line at “x = b”. If ‘f(x)’ is always a positive number, then there’s a shape bounded below by “y = 0”, on the left by “x = a”, on the right by “x = b”, and above by “y = f(x)”. And the definite integral is the area of that enclosed space. If ‘f(x)’ is sometimes zero, then there’s several segments, but their combined area is the definite integral. If ‘f(x)’ is sometimes below zero, then there’s several segments. The definite integral is the sum of the areas of parts above “y = 0” minus the area of the parts below “y = 0”.

(Why say “left boundary” instead of “lower boundary”? Taste, pretty much. But I look at the words “lower boundary” and think about the lower edge, that is, the line where “y = 0” here. And “upper boundary” makes sense as a way to describe the curve where “y = f(x)” as well as “x = b”. I’m confusing enough without making the simple stuff ambiguous.)

Don’t try to pass your thesis defense on this alone. But it’s what you need to understand ‘e’. Start out with the function ‘f’, which has domain of the positive real numbers and range of the positive real numbers. For every ‘x’ in the domain, ‘f(x)’ is the reciprocal, one divided by x. This is a shape you probably know well. It’s a hyperbola. Its asymptotes are the x-axis and the y-axis. It’s a nice gentle curve. Its plot passes through such famous points as (1, 1), (2, 1/2), (1/3, 3), and pairs like that. (10, 1/10) and (1/100, 100) too. ‘f(x)’ is always positive on this domain. Use as left boundary the line “x = 1”. And then — let’s think about different right boundaries.

If the right boundary is close to the left boundary, then this area is tiny. If it’s at, like, “x = 1.1” then the area can’t be more than 0.1. (It’s less than that. If you don’t see why that’s so, fit a rectangle of height 1 and width 0.1 around this curve and these boundaries. See?) But if the right boundary is farther out, this area is more. It’s getting bigger if the right boundary is “x = 2” or “x = 3”. It can get bigger yet. Give me any positive number you like. I can find a right boundary so the area inside this is bigger than your number.

Is there a right boundary where the area is exactly 1? … Well, it’s hard to see how there couldn’t be. If a quantity (“area between x = 1 and x = b”) changes from less than one to greater than one, it’s got to pass through 1, right? … Yes, it does, provided some technical points are true, and in this case they are. So that’s nice.

And there is. It’s a number (settle down, I see you quivering with excitement back there, waiting for me to unveil this) a slight bit more than 2.718. It’s a neat number. Carry it out a couple more digits and it turns out to be 2.718281828. So it looks like a great candidate to memorize. It’s not. It’s an irrational number. The digits go off without repeating or falling into obvious patterns after that. It’s a transcendental number, which has to do with polynomials. Nobody knows whether it’s a normal number, because remember, a normal number is just any real number that you never heard of. To be a normal number, every finite string of digits has to appear in the decimal expansion, just as often as every other string of digits of the same length. We can show by clever counting arguments that roughly every number is normal. Trick is it’s hard to show that any particular number is.

So let me do another definite integral. Set the left boundary to this “x = 2.718281828(etc)”. Set the right boundary a little more than that. The enclosed area is less than 1. Set the right boundary way off to the right. The enclosed area is more than 1. What right boundary makes the enclosed area ‘1’ again? … Well, that will be at about “x = 7.389”. That is, at the square of 2.718281828(etc).

Repeat this. Set the left boundary at “x = (2.718281828etc)2”. Where does the right boundary have to be so the enclosed area is 1? … Did you guess “x = (2.718281828etc)3”? Yeah, of course. You know my rhetorical tricks. What do you want to guess the area is between, oh, “x = (2.718281828etc)3” and “x = (2.718281828etc)5”? (Notice I put a ‘5’ in the superscript there.)

Now, relationships like this will happen with other functions, and with other left- and right-boundaries. But if you want it to work with a function whose rule is as simple as “f(x) = 1 / x”, and areas of 1, then you’re going to end up noticing this 2.718281828(etc). It stands out. It’s worthy of a name.

Which is why this 2.718281828(etc) is a number you’ve heard of. It’s named ‘e’. Leonhard Euler, whom you will remember as having written or proved the fundamental theorem for every area of mathematics ever, gave it that name. He used it first when writing for his own work. Then (in November 1731) in a letter to Christian Goldbach. Finally (in 1763) in his textbook Mechanica. Everyone went along with him because Euler knew how to write about stuff, and how to pick symbols that worked for stuff.

Once you know ‘e’ is there, you start to see it everywhere. In Western mathematics it seems to have been first noticed by Jacob (I) Bernoulli, who noticed it in toy compound interest problems. (Given this, I’d imagine it has to have been noticed by the people who did finance. But I am ignorant of the history of financial calculations. Writers of the kind of pop-mathematics history I read don’t notice them either.) Bernoulli and Pierre Raymond de Montmort noticed the reciprocal of ‘e’ turning up in what we’ve come to call the ‘hat check problem’. A large number of guests all check one hat each. The person checking hats has no idea who anybody is. What is the chance that nobody gets their correct hat back? … That chance is the reciprocal of ‘e’. The number’s about 0.368. In a connected but not identical problem, suppose something has one chance in some number ‘N’ of happening each attempt. And it’s given ‘N’ attempts given for it to happen. What’s the chance that it doesn’t happen? The bigger ‘N’ gets, the closer the chance it doesn’t happen gets to the reciprocal of ‘e’.

It comes up in peculiar ways. In high school or freshman calculus you see it defined as what you get if you take for ever-larger real numbers ‘x’. (This is the toy-compound-interest problem Bernoulli found.) But you can find the number other ways. You can calculate it — if you have the stamina — by working out the value of

There’s a simpler way to write that. There always is. Take all the nonnegative whole numbers — 0, 1, 2, 3, 4, and so on. Take their factorials. That’s 1, 1, 2, 6, 24, and so on. Take the reciprocals of all those. That’s … 1, 1, one-half, one-sixth, one-twenty-fourth, and so on. Add them all together. That’s ‘e’.

This ‘e’ turns up all the time. Any system whose rate of growth depends on its current value has an ‘e’ lurking in its description. That’s true if it declines, too, as long as the decline depends on its current value. It gets stranger. Cross ‘e’ with complex-valued numbers and you get, not just growth or decay, but oscillations. And many problems that are hard to solve to start with become doable, even simple, if you rewrite them as growths and decays and oscillations. Through ‘e’ problems too hard to do become problems of polynomials, or even simpler things.

Simple problems become that too. That property about the area underneath “f(x) = 1/x” between “x = 1” and “x = b” makes ‘e’ such a natural base for logarithms that we call it the base for natural logarithms. Logarithms let us replace multiplication with addition, and division with subtraction, easier work. They change exponentiation problems to multiplication, again easier. It’s a strange touch, a wondrous one.

There are some numbers interesting enough to attract books about them. π, obviously. 0. The base of imaginary numbers, , has a couple. I only know one pop-mathematics treatment of ‘e’, Eli Maor’s e: The Story Of A Number. I believe there’s room for more.

You know, the way anyone’s calculator will let you raise 2 to the 85th power. And then raise 3 to whatever number that is. Anyway. The digits of this will agree with the digits of ‘e’ for the first 18,457,734,525,360,901,453,873,570 decimal digits. One Richard Sabey found that, by what means I do not know, in 2004. The page linked there includes a bunch of other, no less amazing, approximations to numbers like ‘e’ and π and the Euler-Mascheroni Constant.

So I did a bit of thinking. There’s a prosthaphaeretic rule that lets you calculate square roots using nothing more than trigonometric functions. Is there one that lets you calculate cube roots?

And I don’t know. I don’t see where there is one. I may be overlooking an approach, though. Let me outline what I’ve thought out.

If we suppose the number whose square we want is then we can find . The calculation on the right-hand side of this is easy; double your number and subtract one. Then to the lookup table; find the angle whose cosine is that number. That angle is two times θ. So divide that angle in two. Cosine of that is, well, and most people would agree that’s a square root of without any further work.

Why can’t I do the same thing with a triple-angle formula? … Well, here’s my choices among the normal trig functions:

Yes, I see you in the corner, hopping up and down and asking about the cosecant. It’s not any better. Trust me.

So you see the problem here. The number whose cube root I want has to be the . Or the cube of the sine of theta, or the cube of the tangent of theta. Whatever. The trouble is I don’t see a way to calculate cosine (sine, tangent) of 3θ, or 3 times the cosine (etc) of θ. Nor to get some other simple expression out of that. I can get mixtures of the cosine of 3θ plus the cosine of θ, sure. But that doesn’t help me figure out what θ is.

Can it be worked out? Oh, sure, yes. There’s absolutely approximation schemes that would let me find a value of θ which makes true, say,

But: is there a way takes less work than some ordinary method of calculating a cube root? Even if you allow some work to be done by someone else ahead of time, such as by computing a table of trig functions? … If there is, I don’t see it. So there’s another point in favor of logarithms. Finding a cube root using a logarithm table is no harder than finding a square root, or any other root.

If you’re using trig tables, you can find a square root, or a fourth root, or an eighth root. Cube roots, if I’m not missing something, are beyond us. So are, I imagine, fifth roots and sixth roots and seventh roots and so on. I could protest that I have never in my life cared what the seventh root of a thing is, but it would sound like a declaration of sour grapes. Too bad.

If I have missed something, it’s probably obvious. Please go ahead and tell me what it is.

Sunday’s comics post got me thinking about ways to calculate square roots besides using the square root function on a calculator. I wondered if I could find my own little approach. Maybe something that isn’t iterative. Iterative methods are great in that they tend to forgive numerical errors. All numerical calculations carry errors with them. But they can involve a lot of calculation and, in principle, never finish. You just give up when you think the answer is good enough. A non-iterative method carries the promise that things will, someday, end.

And I found one! It’s a neat little way to find the square root of a number between 0 and 1. Call the number ‘S’, as in square. I’ll give you the square root from it. Here’s how.

First, take S. Multiply S by two. Then subtract 1 from this.

Next. Find the angle — I shall call it 2A — whose cosine is this number 2S – 1.

You have 2A? Great. Divide that in two, so that you get the angle A.

Now take the cosine of A. This will be the (positive) square root of S. (You can find the negative square root by taking minus this.)

Let me show it in action. Let’s say you want the square root of 0.25. So let S = 0.25. And then 2S – 1 is two times 0.25 (which is 0.50) minus 1. That’s -0.50. What angle has cosine of -0.50? Well, that’s an angle of 2 π / 3 radians. Mathematicians think in radians. People think in degrees. And you can do that too. This is 120 degrees. Divide this by two. That’s an angle of π / 3 radians, or 60 degrees. The cosine of π / 3 is 0.5. And, indeed, 0.5 is the square root of 0.25.

I hear you protesting already: what if we want the square root of something larger than 1? Like, how is this any good in finding the square root of 81? Well, if we add a little step before and after this work, we’re in good shape. Here’s what.

So we start with some number larger than 1. Say, 81. Fine. Divide it by 100. If it’s still larger than 100, divide it again, and again, until you get a number smaller than 1. Keep track of how many times you did this. In this case, 81 just has to be divided by 100 the one time. That gives us 0.81, a number which is smaller than 1.

Twice 0.81 minus 1 is equal to 0.62. The angle which has 0.81 as cosine is roughly 0.90205. Half this angle is about 0.45103. And the cosine of 0.45103 is 0.9. This is looking good, but obviously 0.9 is no square root of 81.

Ah, but? We divided 81 by 100 to get it smaller than 1. So we balance that by multiplying 0.9 by 10 to get it back larger than 1. If we had divided by 100 twice to start with, we’d multiply by 10 twice to finish. If we had divided by 100 six times to start with, we’d multiply by 10 six times to finish. Yes, 10 is the square root of 100. You see what’s going on here.

(And if you want the square root of a tiny number, something smaller than 0.01, it’s not a bad idea to multiply it by 100, maybe several times over. Then calculate the square root, and divide the result by 10 a matching number of times. It’s hard to calculate with very big or with very small numbers. If you must calculate, do it on very medium numbers. This is one of those little things you learn in numerical mathematics.)

So maybe now you’re convinced this works. You may not be convinced of why this works. What I’m using here is a trigonometric identity, one of the angle-doubling formulas. Its heart is this identity. It’s familiar to students whose Intro to Trigonometry class is making them finally, irrecoverably hate mathematics:

Here, I let ‘S’ be the squared number, . So then anything I do to find gets me the square root. The algebra here is straightforward. Since ‘S’ is that cosine-squared thing, all I have to do is double it, subtract one, and then find what angle 2θ has that number as cosine. Then the cosine of θ has to be the square root.

Oh, yeah, all right. There’s an extra little objection. In what world is it easier to take an arc-cosine (to figure out what 2θ is) and then later to take a cosine? … And the answer is, well, any world where you’ve already got a table printed out of cosines of angles and don’t have a calculator on hand. This would be a common condition through to about 1975. And not all that ridiculous through to about 1990.

This is an example of a prosthaphaeretic rule. These are calculation tools. They’re used to convert multiplication or division problems into addition and subtraction. The idea is exactly like that of logarithms and exponents. Using trig functions predates logarithms. People knew about sines and cosines long before they knew about logarithms and exponentials. But the impulse is the same. And you might, if you squint, see in my little method here an echo of what you’d do more easily with a logarithm table. If you had a log table, you’d calculate instead. But if you don’t have a log table, and only have a table of cosines, you can calculate at least.

Is this easier than normal methods of finding square roots? … If you have a table of cosines, yes. Definitely. You have to scale the number into range (divide by 100 some) do an easy multiplication (S times 2), an easy subtraction (minus 1), a table lookup (arccosine), an easy division (divide by 2), another table lookup (cosine), and scale the number up again (multiply by 10 some). That’s all. Seven steps, and two of them are reading. Two of the rest are multiplying or dividing by 10’s. Using logarithm tables has it beat, yes, at five steps (two that are scaling, two that are reading, one that’s dividing by 2). But if you can’t find your table of logarithms, and do have a table of cosines, you’re set.

This may not be practical, since who has a table of cosines anymore? Who hasn’t also got a calculator that does square roots faster? But it delighted me to work this scheme out. Give me a while and maybe I’ll think about cube roots.

My car’s odometer first read 9 on my final test drive before buying it, in June of 2009. It flipped over to 10 barely a minute after that, somewhere near Jersey Freeze ice cream parlor at what used to be the Freehold Traffic Circle. Ask a Central New Jersey person of sufficient vintage about that place. Its odometer read 90 miles sometime that weekend, I think while I was driving to The Book Garden on Route 537. Ask a Central New Jersey person of sufficient reading habits about that place. It’s still there. It flipped over to 100 sometime when I was driving back later that day.

The odometer read 900 about two months after that, probably while I was driving to work, as I had a longer commute in those days. It flipped over to 1000 a couple days after that. The odometer first read 9,000 miles sometime in spring of 2010 and I don’t remember what I was driving to for that. It flipped over from 9,999 to 10,000 miles several weeks later, as I pulled into the car dealership for its scheduled servicing. Yes, this kind of impressed the dealer that I got there exactly on the round number.

The odometer first read 90,000 in late August of last year, as I was driving to some competitive pinball event in western Michigan. It’s scheduled to flip over to 100,000 miles sometime this week as I get to the dealer for its scheduled maintenance. While cars have gotten to be much more reliable and durable than they used to be, the odometer will never flip over to 900,000 miles. At least I can’t imagine owning it long enough, at my rate of driving the past eight years, that this would ever happen. It’s hard to imagine living long enough for the car to reach 900,000 miles. Thursday or Friday it should flip over to 100,000 miles. The leading digit on the odometer will be 1 or, possibly, 2 for the rest of my association with it.

The point of this little autobiography is this observation. Imagine all the days that I have owned this car, from sometime in June 2009 to whatever day I sell, lose, or replace it. Pick one. What is the leading digit of my odometer on that day? It could be anything from 1 to 9. But it’s more likely to be 1 than it is 9. Right now it’s as likely to be any of the digits. But after this week the chance of ‘1’ being the leading digit will rise, and become quite more likely than that of ‘9’. And it’ll never lose that edge.

This is a reflection of Benford’s Law. It is named, as most mathematical things are, imperfectly. The law-namer was Frank Benford, a physicist, who in 1938 published a paper The Law Of Anomalous Numbers. It confirmed the observation of Simon Newcomb. Newcomb was a 19th century astronomer and mathematician of an exhausting number of observations and developments. Newcomb observed the logarithm tables that anyone who needed to compute referred to often. The earlier pages were more worn-out and dirty and damaged than the later pages. People worked with numbers that start with ‘1’ more than they did numbers starting with ‘2’. And more those that start ‘2’ than start ‘3’. More that start with ‘3’ than start with ‘4’. And on. Benford showed this was not some fluke of calculations. It turned up in bizarre collections of data. The surface areas of rivers. The populations of thousands of United States municipalities. Molecular weights. The digits that turned up in an issue of Reader’s Digest. There is a bias in the world toward numbers that start with ‘1’.

And this is, prima facie, crazy. How can the surface areas of rivers somehow prefer to be, say, 100-199 hectares instead of 500-599 hectares? A hundred is a human construct. (Indeed, it’s many human constructs.) That we think ten is an interesting number is an artefact of our society. To think that 100 is a nice round number and that, say, 81 or 144 are not is a cultural choice. Grant that the digits of street addresses of people listed in American Men of Science — one of Benford’s data sources — have some cultural bias. How can another of his sources, molecular weights, possibly?

The bias sneaks in subtly. Don’t they all? It lurks at the edge of the table of data. The table header, perhaps, where it says “River Name” and “Surface Area (sq km)”. Or at the bottom where it says “Length (miles)”. Or it’s never explicit, because I take for granted people know my car’s mileage is measured in miles.

What would be different in my introduction if my car were Canadian, and the odometer measured kilometers instead? … Well, I’d not have driven the 9th kilometer; someone else doing a test-drive would have. The 90th through 99th kilometers would have come a little earlier that first weekend. The 900th through 999th kilometers too. I would have passed the 99,999th kilometer years ago. In kilometers my car has been in the 100,000s for something like four years now. It’s less absurd that it could reach the 900,000th kilometer in my lifetime, but that still won’t happen.

What would be different is the precise dates about when my car reached its milestones, and the amount of days it spent in the 1’s and the 2’s and the 3’s and so on. But the proportions? What fraction of its days it spends with a 1 as the leading digit versus a 2 or a 5? … Well, that’s changed a little bit. There is some final mile, or kilometer, my car will ever register and it makes a little difference whether that’s 239,000 or 385,000. But it’s only a little difference. It’s the difference in how many times a tossed coin comes up heads on the first 1,000 flips versus the second 1,000 flips. They’ll be different numbers, but not that different.

What’s the difference between a mile and a kilometer? A mile is longer than a kilometer, but that’s it. They measure the same kinds of things. You can convert a measurement in miles to one in kilometers by multiplying by a constant. We could as well measure my car’s odometer in meters, or inches, or parsecs, or lengths of football fields. The difference is what number we multiply the original measurement by. We call this “scaling”.

Whatever we measure, in whatever unit we measure, has to have a leading digit of something. So it’s got to have some chance of starting out with a ‘1’, some chance of starting out with a ‘2’, some chance of starting out with a ‘3’, and so on. But that chance can’t depend on the scale. Measuring something in smaller or larger units doesn’t change the proportion of how often each leading digit is there.

These facts combine to imply that leading digits follow a logarithmic-scale law. The leading digit should be a ‘1’ something like 30 percent of the time. And a ‘2’ about 18 percent of the time. A ‘3’ about one-eighth of the time. And it decreases from there. ‘9’ gets to take the lead a meager 4.6 percent of the time.

Roughly. It’s not going to be so all the time. Measure the heights of humans in meters and there’ll be far more leading digits of ‘1’ than we should expect, as most people are between 1 and 2 meters tall. Measure them in feet and ‘5’ and ‘6’ take a great lead. The law works best when data can sprawl over many orders of magnitude. If we lived in a world where people could as easily be two inches as two hundred feet tall, Benford’s Law would make more accurate predictions about their heights. That something is a mathematical truth does not mean it’s independent of all reason.

For example, the reader thinking back some may be wondering: granted that atomic weights and river areas and populations carry units with them that create this distribution. How do street addresses, one of Benford’s observed sources, carry any unit? Well, street addresses are, at least in the United States custom, a loose measure of distance. The 100 block (for example) of a street is within one … block … from whatever the more important street or river crossing that street is. The 900 block is farther away.

This extends further. Block numbers are proxies for distance from the major cross feature. House numbers on the block are proxies for distance from the start of the block. We have a better chance to see street number 419 than 1419, to see 419 than 489, or to see 419 than to see 1489. We can look at Benford’s Law in the second and third and other minor digits of numbers. But we have to be more cautious. There is more room for variation and quirk events. A block-filling building in the downtown area can take whatever street number the owners think most auspicious. Smaller samples of anything are less predictable.

Nevertheless, Benford’s Law has become famous to forensic accountants the past several decades, if we allow the use of the word “famous” in this context. But its fame is thanks to the economists Hal Varian and Mark Nigrini. They observed that real-world financial data should be expected to follow this same distribution. If they don’t, then there might be something suspicious going on. This is not an ironclad rule. There might be good reasons for the discrepancy. If your work trips are always to the same location, and always for one week, and there’s one hotel it makes sense to stay at, and you always learn you’ll need to make the trips about one month ahead of time, of course the hotel bill will be roughly the same. Benford’s Law is a simple, rough tool, a way to decide what data to scrutinize for mischief. With this in mind I trust none of my readers will make the obvious leading-digit mistake when padding their expense accounts anymore.

Since I’ve done you that favor, anyone out there think they can pick me up at the dealer’s Thursday, maybe Friday? Thanks in advance.

Learning of imaginary numbers, things created to be the square roots of negative numbers, inspired me. It probably inspires anyone who’s the sort of person who’d become a mathematician. The trick was great. I wondered could I do it? Could I find some other useful expansion of the number system?

The square root of a complex-valued number sounded like the obvious way to go, until a little later that week when I learned that’s just some other complex-valued numbers. The next thing I hit on: how about the logarithm of a negative number? Couldn’t that be a useful expansion of numbers?

No. It turns out you can make a sensible logarithm of negative, and complex-valued, numbers using complex-valued numbers. Same with trigonometric and inverse trig functions, tangents and arccosines and all that. There isn’t anything we can do with the normal mathematical operations that needs something bigger than the complex-valued numbers to play with. It’s possible to expand on the complex-valued numbers. We can make quaternions and some more elaborate constructs there. They don’t solve any particular shortcoming in complex-valued numbers, but they’ve got their uses. I never got anywhere near reinventing them. I don’t regret the time spent on that. There’s something useful in trying to invent something even if it fails.

One problem with mathematics — with all intellectual fields, really — is that it’s easy, when teaching, to give the impression that this stuff is the Word of God, built into the nature of the universe and inarguable. It’s so not. The stuff we find interesting and how we describe those things are the results of human thought, attempts to say what is interesting about a thing and what is useful. And what best approximates our ideas of what we would like to know. So I was happy to see this come across my Twitter feed:

Some background on Euler, Leibniz, Bernoulli and the controversy about logs of negative numbers. https://t.co/MZAJ6LkTwX

The links to a 12-page paper by Deepak Bal, Leibniz, Bernoulli, and the Logarithms of Negative Numbers. It’s a review of how the idea of a logarithm of a negative number got developed over the course of the 18th century. And what great minds, like Gottfried Leibniz and John (I) Bernoulli argued about as they find problems with the implications of what they were doing. (There were a lot of Bernoullis doing great mathematics, and even multiple John Bernoullis. The (I) is among the ways we keep them sorted out.) It’s worth a read, I think, even if you’re not all that versed in how to calculate logarithms. (but if you’d like to be better-versed, here’s the tail end of some thoughts about that.) The process of how a good idea like this comes to be is worth knowing.

Also: it turns out there’s not “the” logarithm of a complex-valued number. There’s infinitely many logarithms. But they’re a family, all strikingly similar, so we can pick one that’s convenient and just use that. Ask if you’re really interested.

Now to close out what Comic Strip Master Command sent my way through last Saturday. And I’m glad I’ve shifted to a regular schedule for these. They ordered a mass of comics with mathematical themes for Sunday and Monday this current week.

Karen Montague-Reyes’s Clear Blue Water rerun for the 17th describes trick-or-treating as “logarithmic”. The intention is to say that the difficulty in wrangling kids from house to house grows incredibly fast as the number of kids increases. Fair enough, but should it be “logarithmic” or “exponential”? Because the logarithm grows slowly as the number you take the logarithm of grows. It grows all the slower the bigger the number gets. The exponential of a number, though, that grows faster and faster still as the number underlying it grows. So is this mistaken?

I say no. It depends what the logarithm is, and is of. If the number of kids is the logarithm of the difficulty of hauling them around, then the intent and the mathematics are in perfect alignment. Five kids are (let’s say) ten times harder to deal with than four kids. Sensible and, from what I can tell of packs of kids, correct.

Rick Detorie’s One Big Happy for the 17th of January, 2017. The section was about how the appearance and trappings of wealth matter for more than the actual substance of wealth so everyone’s really up to speed in the course.

Rick Detorie’s One Big Happy for the 17th is a resisting-the-word-problem joke. There’s probably some warning that could be drawn about this in how to write story problems. It’s hard to foresee all the reasonable confounding factors that might get a student to the wrong answer, or to see a problem that isn’t meant to be there.

Bill Holbrook’s On The Fastrack for the 19th continues Fi’s story of considering leaving Fastrack Inc, and finding a non-competition clause that’s of appropriate comical absurdity. As an auditor there’s not even a chance Fi could do without numbers. Were she a pure mathematician … yeah, no. There’s fields of mathematics in which numbers aren’t all that important. But we never do without them entirely. Even if we exclude cases where a number is just used as an index, for which Roman numerals would be almost as good as regular numerals. If nothing else numbers would keep sneaking in by way of polynomials.

Bill Holbrook’s On The Fastrack for the 19th of January, 2017. I feel like someone could write a convoluted story that lets someone do mathematics while avoiding any actual use of any numbers, and that it would probably be Greg Egan who did it.

Mort Walker and Dik Browne’s Vintage Hi and Lois for the 27th of July, 1959 uses calculus as stand-in for what college is all about. Lois’s particular example is about a second derivative. Suppose we have a function named ‘y’ and that depends on a variable named ‘x’. Probably it’s a function with domain and range both real numbers. If complex numbers were involved then the variable would more likely be called ‘z’. The first derivative of a function is about how fast its values change with small changes in the variable. The second derivative is about how fast the values of the first derivative change with small changes in the variable.

Mort Walker and Dik Browne’s Vintage Hi and Lois for the 27th of July, 1959. Fortunately Lois discovered the other way to avoid college costs: simply freeze the ages of your children where they are now, so they never face student loans. It’s an appealing plan until you imagine being Trixie.

The ‘d’ in this equation is more of an instruction than it is a number, which is why it’s a mistake to just divide those out. Instead of writing it as it’s permitted, and common, to write it as . This means the same thing. I like that because, to me at least, it more clearly suggests “do this thing (take the second derivative) to the function we call ‘y’.” That’s a matter of style and what the author thinks needs emphasis.

There are infinitely many possible functions y that would make the equation true. They all belong to one family, though. They all look like , where ‘C’ and ‘D’ are some fixed numbers. There’s no way to know, from what Lois has given, what those numbers should be. It might be that the context of the problem gives information to use to say what those numbers should be. It might be that the problem doesn’t care what those numbers should be. Impossible to say without the context.

There were a couple of rerun comics in this week’s roundup, so I’ll go with that theme. And I’ll put in one more appeal for subjects for my End of 2016 Mathematics A To Z. Have a mathematics term you’d like to see me go on about? Just ask! Much of the alphabet is still available.

John Kovaleski’s Bo Nanas rerun the 24th is about probability. There’s something wondrous and strange that happens when we talk about the probability of things like birth days. They are, if they’re in the past, determined and fixed things. The current day is also a known, determined, fixed thing. But we do mean something when we say there’s a 1-in-365 (or 366, or 365.25 if you like) chance of today being your birthday. It seems to me this is probability based on ignorance. If you don’t know when my birthday is then your best guess is to suppose there’s a one-in-365 (or so) chance that it’s today. But I know when my birthday is; to me, with this information, the chance today is my birthday is either 0 or 1. But what are the chances that today is a day when the chance it’s my birthday is 1? At this point I realize I need much more training in the philosophy of mathematics, and the philosophy of probability. If someone is aware of a good introductory book about it, or a web site or blog that goes into these problems in a way a lay reader will understand, I’d love to hear of it.

I’ve featured this installment of Poor Richard’s Almanac before. I’ll surely feature it again. I like Richard Thompson’s sense of humor. The first panel mentions non-Euclidean geometry, using the connotation that it does have. Non-Euclidean geometries are treated as these magic things — more, these sinister magic things — that defy all reason. They can’t defy reason, of course. And at least some of them are even sensible if we imagine we’re drawing things on the surface of the Earth, or at least the surface of a balloon. (There are non-Euclidean geometries that don’t look like surfaces of spheres.) They don’t work exactly like the geometry of stuff we draw on paper, or the way we fit things in rooms. But they’re not magic, not most of them.

Stephen Bentley’s Herb and Jamaal for the 25th I believe is a rerun. I admit I’m not certain, but it feels like one. (Bentley runs a lot of unannounced reruns.) Anyway I’m refreshed to see a teacher giving a student permission to count on fingers if that’s what she needs to work out the problem. Sometimes we have to fall back on the non-elegant ways to get comfortable with a method.

Dave Whamond’s Reality Check for the 25th name-drops Einstein and one of the three equations that has any pop-culture currency.

Guy Gilchrist’s Today’s Dogg for the 27th is your basic mathematical-symbols joke. We need a certain number of these.

Berkeley Breathed’s Bloom County for the 28th is another rerun, from 1981. And it’s been featured here before too. As mentioned then, Milo is using calculus and logarithms correctly in his rather needless insult of Freida. 10,000 is a constant number, and as mentioned a few weeks back its derivative must be zero. Ten to the power of zero is 1. The log of 10, if we’re using logarithms base ten, is also 1. There are many kinds of logarithms but back in 1981, the default if someone said “log” would be the logarithm base ten. Today the default is more muddled; a normal person would mean the base-ten logarithm by “log”. A mathematician might mean the natural logarithm, base ‘e’, by “log”. But why would a normal person mention logarithms at all anymore?

Jef Mallett’s Frazz for the 28th is mostly a bit of wordplay on evens and odds. It’s marginal, but I do want to point out some comics that aren’t reruns in this batch.

Today’s mathematics glossary term is another one requested by Jacob Kanev. Kaven, I learned last time, has got a blog, “Some Unconsidered Trifles”, for those interested in having more things to read. Kanev’s request this time was a term new to me. But learning things I didn’t expect to consider is part of the fun of this dance.

Kullback-Leibler Divergence.

The Kullback-Leibler Divergence comes to us from information theory. It’s also known as “information divergence” or “relative entropy”. Entropy is by now a familiar friend. We got to know it through, among other things, the “How interesting is a basketball tournament?” question. In this context, entropy is a measure of how surprising it would be to know which of several possible outcomes happens. A sure thing has an entropy of zero; there’s no potential surprise in it. If there are two equally likely outcomes, then the entropy is 1. If there are four equally likely outcomes, then the entropy is 2. If there are four possible outcomes, but one is very likely and the other three mediocre, the entropy might be low, say, 0.5 or so. It’s mostly but not perfectly predictable.

Suppose we have a set of possible outcomes for something. (Pick anything you like. It could be the outcomes of a basketball tournament. It could be how much a favored stock rises or falls over the day. It could be how long your ride into work takes. As long as there are different possible outcomes, we have something workable.) If we have a probability, a measure of how likely each of the different outcomes is, then we have a probability distribution. More likely things have probabilities closer to 1. Less likely things have probabilities closer to 0. No probability is less than zero or more than 1. All the probabilities added together sum up to 1. (These are the rules which make something a probability distribution, not just a bunch of numbers we had in the junk drawer.)

The Kullback-Leibler Divergence describes how similar two probability distributions are to one another. Let me call one of these probability distributions p. I’ll call the other one q. We have some number of possible outcomes, and we’ll use k as an index for them. pk is how likely, in distribution p, that outcome number k is. qk is how likely, in distribution q, that outcome number k is.

To calculate this divergence, we work out, for each k, the number pk times the logarithm of pk divided by qk. Here the logarithm is base two. Calculate all this for every one of the possible outcomes, and add it together. This will be some number that’s at least zero, but it might be larger.

The closer that distribution p and distribution q are to each other, the smaller this number is. If they’re exactly the same, this number will be zero. The less that distribution p and distribution q are like each other, the bigger this number is.

And that’s all good fun, but, why bother with it? And at least one answer I can give is that it lets us measure how good a model of something is.

Suppose we think we have an explanation for how something varies. We can say how likely it is we think there’ll be each of the possible different outcomes. This gives us a probability distribution which let’s call q. We can compare that to actual data. Watch whatever it is for a while, and measure how often each of the different possible outcomes actually does happen. This gives us a probability distribution which let’s call p.

If our model is a good one, then the Kullback-Leibler Divergence between p and q will be small. If our model’s a lousy one, then this divergence will be large. If we have a couple different models, we can see which ones make for smaller divergences and which ones make for larger divergences. Probably we’ll want smaller divergences.

Here you might ask: why do we need a model? Isn’t the actual data the best model we might have? It’s a fair question. But no, real data is kind of lousy. It’s all messy. It’s complicated. We get extraneous little bits of nonsense clogging it up. And the next batch of results is going to be different from the old ones anyway, because real data always varies.

Furthermore, one of the purposes of a model is to be simpler than reality. A model should do away with complications so that it is easier to analyze, easier to make predictions with, and easier to teach than the reality is. But a model mustn’t be so simple that it can’t represent important aspects of the thing we want to study.

The Kullback-Leibler Divergence is a tool that we can use to quantify how much better one model or another fits our data. It also lets us quantify how much of the grit of reality we lose in our model. And this is at least some of the use of this quantity.

An isomorphism is a kind of homomorphism. And a homomorphism is a kind of thing we do with groups. A group is a mathematical construct made up of two things. One is a set of things. The other is an operation, like addition, where we take two of the things and get one of the things in the set. I think that’s as far as we need to go in this chain of defining things.

A homomorphism is a mapping, or if you like the word better, a function. The homomorphism matches everything in a group to the things in a group. It might be the same group; it might be a different group. What makes it a homomorphism is that it preserves addition.

I gave an example last time, with groups I called G and H. G had as its set the whole numbers 0 through 3 and as operation addition modulo 4. H had as its set the whole numbers 0 through 7 and as operation addition modulo 8. And I defined a homomorphism φ which took a number in G and matched it the number in H which was twice that. Then for any a and b which were in G’s set, φ(a + b) was equal to φ(a) + φ(b).

We can have all kinds of homomorphisms. For example, imagine my new φ1. It takes whatever you start with in G and maps it to the 0 inside H. φ1(1) = 0, φ1(2) = 0, φ1(3) = 0, φ1(0) = 0. It’s a legitimate homomorphism. Seems like it’s wasting a lot of what’s in H, though.

An isomorphism doesn’t waste anything that’s in H. It’s a homomorphism in which everything in G’s set matches to exactly one thing in H’s, and vice-versa. That is, it’s both a homomorphism and a bijection, to use one of the terms from the Summer 2015 A To Z. The key to remembering this is the “iso” prefix. It comes from the Greek “isos”, meaning “equal”. You can often understand an isomorphism from group G to group H showing how they’re the same thing. They might be represented differently, but they’re equivalent in the lights you use.

I can’t make an isomorphism between the G and the H I started with. Their sets are different sizes. There’s no matching everything in H’s set to everything in G’s set without some duplication. But we can make other examples.

For instance, let me start with a new group G. It’s got as its set the positive real numbers. And it has as its operation ordinary multiplication, the kind you always do. And I want a new group H. It’s got as its set all the real numbers, positive and negative. It has as its operation ordinary addition, the kind you always do.

For an isomorphism φ, take the number x that’s in G’s set. Match it to the number that’s the logarithm of x, found in H’s set. This is a one-to-one pairing: if the logarithm of x equals the logarithm of y, then x has to equal y. And it covers everything: all the positive real numbers have a logarithm, somewhere in the positive or negative real numbers.

And this is a homomorphism. Take any x and y that are in G’s set. Their “addition”, the group operation, is to multiply them together. So “x + y”, in G, gives us the number xy. (I know, I know. But trust me.) φ(x + y) is equal to log(xy), which equals log(x) + log(y), which is the same number as φ(x) + φ(y). There’s a way to see the postive real numbers being multiplied together as equivalent to all the real numbers being added together.

You might figure that the positive real numbers and all the real numbers aren’t very different-looking things. Perhaps so. Here’s another example I like, drawn from Wikipedia’s entry on Isomorphism. It has as sets things that don’t seem to have anything to do with one another.

Let me have another brand-new group G. It has as its set the whole numbers 0, 1, 2, 3, 4, and 5. Its operation is addition modulo 6. So 2 + 2 is 4, while 2 + 3 is 5, and 2 + 4 is 0, and 2 + 5 is 1, and so on. You get the pattern, I hope.

The brand-new group H, now, that has a more complicated-looking set. Its set is ordered pairs of whole numbers, which I’ll represent as (a, b). Here ‘a’ may be either 0 or 1. ‘b’ may be 0, 1, or 2. To describe its addition rule, let me say we have the elements (a, b) and (c, d). Find their sum first by adding together a and c, modulo 2. So 0 + 0 is 0, 1 + 0 is 1, 0 + 1 is 1, and 1 + 1 is 0. That result is the first number in the pair. The second number we find by adding together b and d, modulo 3. So 1 + 0 is 1, and 1 + 1 is 2, and 1 + 2 is 0, and so on.

So, for example, (0, 1) plus (1, 1) will be (1, 2). But (0, 1) plus (1, 2) will be (1, 0). (1, 2) plus (1, 0) will be (0, 2). (1, 2) plus (1, 2) will be (0, 1). And so on.

The isomorphism matches up things in G to things in H this way:

In G

φ(G), in H

0

(0, 0)

1

(1, 1)

2

(0, 2)

3

(1, 0)

4

(0, 1)

5

(1, 2)

I recommend playing with this a while. Pick any pair of numbers x and y that you like from G. And check their matching ordered pairs φ(x) and φ(y) in H. φ(x + y) is the same thing as φ(x) + φ(y) even though the things in G’s set don’t look anything like the things in H’s.

Isomorphisms exist for other structures. The idea extends the way homomorphisms do. A ring, for example, has two operations which we think of as addition and multiplication. An isomorphism matches two rings in ways that preserve the addition and multiplication, and which match everything in the first ring’s set to everything in the second ring’s set, one-to-one. The idea of the isomorphism is that two different things can be paired up so that they look, and work, remarkably like one another.

One of the common uses of isomorphisms is describing the evolution of systems. We often like to look at how some physical system develops from different starting conditions. If you make a little variation in how things start, does this produce a small change in how it develops, or does it produce a big change? How big? And the description of how time changes the system is, often, an isomorphism.

Isomorphisms also appear when we study the structures of groups. They turn up naturally when we look at things called “normal subgroups”. The name alone gives you a good idea what a “subgroup” is. “Normal”, well, that’ll be another essay.

The next exhibit on the Set Tour here builds on a couple of the previous ones. First is the set Sn, that is, the surface of a hypersphere in n+1 dimensions. Second is Bn, the ball — the interior — of a hypersphere in n dimensions. Yeah, it bugs me too that Sn isn’t the surface of Bn. But it’d be too much work to change things now. The third has lurked implicitly since all the way back to Rn, a set of n real numbers for which the ordering of the numbers matters. (That is, that the set of numbers 2, 3 probably means something different than the set 3, 2.) And fourth is a bit of writing we picked up with matrices. The selection is also dubiously relevant to my own thesis from back in the day.

Sn x m and Bn x m

Here ‘n’ and ‘m’ are whole numbers, and I’m not saying which ones because I don’t need to tie myself down. Just as with Rn and with matrices this is a whole family of sets. Each different pair of n and m gives us a different set Sn x m or Bn x m, but they’ll all look quite similar.

The multiplication symbol here is a kind of multiplication, just as it was in matrices. That kind is called a “direct product”. What we mean by Sn x m is that we have a collection of items. We have the number m of them. Each one of those items is in Sn. That’s the surface of the hypersphere in n+1 dimensions. And we want to keep track of the order of things; we can’t swap items around and suppose they mean the same thing.

So suppose I write S2 x 7. This is an ordered collection of seven items, every one of which is on the surface of a three-dimensional sphere. That is, it’s the location of seven spots on the surface of the Earth. S2 x 8 offers similar prospects for talking about the location of eight spots.

With that written out, you should have a guess what Bn x m means. Your guess is correct. It’s a collection of m things, each of them within the interior of the n-dimensional ball.

Now the dubious relevance to my thesis. My problem was modeling a specific layer of planetary atmospheres. The model used for this was to pretend the atmosphere was made up of some large number of vortices, of whirlpools. Just like you see in the water when you slide your hand through the water and watch the little whirlpools behind you. The winds could be worked out as the sum of the winds produced by all these little vortices.

In the model, each of these vortices was confined to a single distance from the center of the planet. That’s close enough to true for planetary atmospheres. A layer in the atmosphere is not thick at all, compared to the planet. So every one of these vortices could be represented as a point in S2, the surface of a three-dimensional sphere. There would be some large number of these points. Most of my work used a nice round 256 points. So my model of a planetary atmosphere represented the system as a point in the domain S2 x 256. I was particularly interested in the energy of this set of 256 vortices. That was a function which had, as its domain, S2 x 256, and as range, the real numbers R.

But the connection to my actual work is dubious. I was doing numerical work, for the most part. I don’t think my advisor or I ever wrote S2 x 256 or anything like that when working out what I ought to do, much less what I actually did. Had I done a more analytic thesis I’d surely have needed to name this set. But I didn’t. It was lurking there behind my work nevertheless.

The energy of this system of vortices looked a lot like the potential energy for a bunch of planets attracting each other gravitationally, or like point charges repelling each other electrically. We work it out by looking at each pair of vortices. Work out the potential energy of those two vortices being that strong and that far apart. We call that a pairwise interaction. Then add up all the pairwise interactions. That’s it. [1] The pairwise interaction is stronger as each vortex is stronger; it gets weaker as the vortices get farther apart.

In gravity or electricity problems the strength falls off as the reciprocal of the distance between points. In vortices, the strength falls off as minus one times the logarithm of the distance between points. That’s a difference, and it meant that a lot of analytical results known for electric charges didn’t apply to my problem exactly. That was all right. I didn’t need many. But it does mean that I was fibbing up above, when I said I was working with S2 x 256. Pause a moment. Do you see what the fib was?

I’ll put what would otherwise be a footnote here so folks have a harder time reading right through to the answer.

[1] Physics majors may be saying something like: “wait, I see how this would be the potential energy of these 256 vortices, but where’s the kinetic energy?” The answer is, there is none. It’s all potential energy. The dynamics of point vortices are weird. I didn’t have enough grounding in mechanics when I went into them.

That’s all to the footnote.

Here’s where the fib comes in. If I’m really picking sets of vortices from all of the set S2 x 256, then, can two of them be in the exact same place? Sure they can. Why couldn’t they? For precedent, consider R3. In the three-dimensional vectors I can have the first and third numbers “overlap” and have the same value: (1, 2, 1) is a perfectly good vector. Why would that be different for an ordered set of points on the surface of the sphere? Why can’t vortex 1 and vortex 3 happen to have the same value in S2?

The problem is if two vortices were in the exact same position then the energy would be infinitely large. That’s not unique to vortices. It would be true for masses and gravity, or electric charges, if they were brought perfectly on top of each other. Infinitely large energies are a problem. We really don’t want to deal with them.

We could deal with this by pretending it doesn’t happen. Imagine if you dropped 256 poker chips across the whole surface of the Earth. Would you expect any two to be on top of each other? Would you expect two to be exactly and perfectly on top of each other, neither one even slightly overhanging the other? That’s so unlikely you could safely ignore it, for the same reason you could ignore the chance you’ll toss a coin and have it come up tails 56 times in a row.

And if you were interested in modeling the vortices moving it would be incredibly unlikely to have one vortex collide with another. They’d circle around each other, very fast, almost certainly. So ignoring the problem is defensible in this case.

Or we could be proper and responsible and say, “no overlaps” and “no collisions”. We would define some set that represents “all the possible overlaps and arrangements that give us a collision”. Then we’d say we’re looking at S2 x 256 except for those. I don’t think there’s a standard convention for “all the possible overlaps and collisions”, but Ω is a reasonable choice. Then our domain would be S2 x 256 \ Ω. The backslash means “except for the stuff after this”. This might seem unsatisfying. We don’t explicitly say what combinations we’re excluding. But go ahead and try listing all the combinations that would produce trouble. Try something simple, like S2 x 4. This is why we hide all the complicated stuff under a couple ordinary sentences.

It’s not hard to describe “no overlaps” mathematically. (You would say something like “vortex number j and vortex number k are not at the same position”, with maybe a rider of “unless j and k are the same number”. Or you’d put it in symbols that mean the same thing.) “No collisions” is harder. For gravity or electric charge problems we can describe at least some of them. And I realize now I’m not sure if there is an easy way to describe vortices that collide. I have difficulty imagining how they might, since vortices that are close to one another are pushing each other sideways quite intently. I don’t think that I can say they can’t, though. Not without more thought.